The global market for AI Blind Spot Detection (BSD) systems in commercial vehicles is poised for transformative growth, projected to expand from an estimated $1.2–1.5 billion in 2023 to $4–6 billion by 2030. This surge is primarily driven by the European Union’s General Safety Regulation (GSR), which mandates advanced safety features, including BSD-related functions, for all new commercial vehicles starting July 2024. The GSR is creating a regulatory blueprint that is accelerating similar mandates globally.

Technologically, the market is rapidly evolving from standalone systems toward integrated, intelligent safety domains enabled by sensor fusion (camera + radar). At the same time, the business model is shifting from pure hardware sales to recurring revenue streams from software and services.

This report provides a comprehensive analysis for investors, OEMs, and suppliers, highlighting that successful strategic positioning in this market requires a focus on regulatory foresight, technological integration, and adaptable business models.

Introduction: The Imperative for Smarter Vehicle Safety

The operational environment for commercial vehicles in urban areas is becoming increasingly complex, characterized by mixed traffic and a growing number of Vulnerable Road Users (VRUs) such as cyclists and pedestrians. Traditional mirrors and basic sensors are insufficient to address the critical challenge of blind spots, which remain a leading contributor to serious collisions.

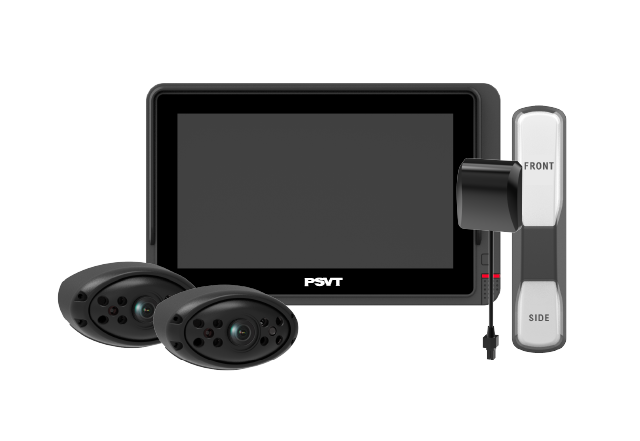

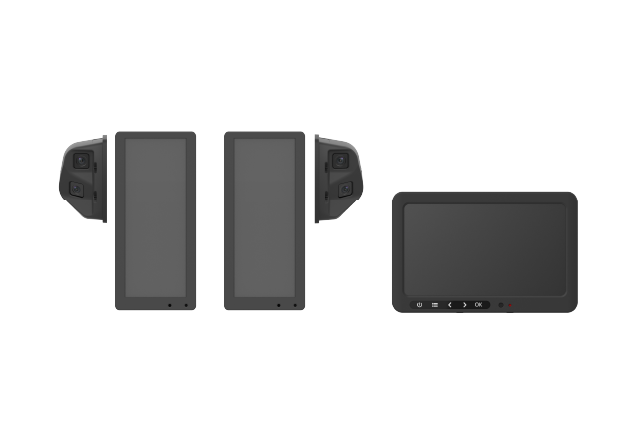

AI-powered Blind Spot Detection systems represent a technological leap. By leveraging advanced algorithms, these systems do not merely detect objects; they classify them (e.g., pedestrian, cyclist) and assess potential risks in real time. This shift from passive monitoring to active intervention is fundamental and closely aligned with global “Vision Zero” policies aimed at eliminating road fatalities and serious injuries.

This analysis examines the regulatory, technological, and market forces driving the adoption of these intelligent systems.

Primary Growth Driver: The Regulatory Catalyst

Regulatory mandates are the single most powerful force propelling the AI BSD market. The EU General Safety Regulation (GSR – EU 2019/2144) is the cornerstone of this movement, establishing a clear, phased timeline for mandatory adoption.

- Key Timeline: The GSR requires Blind Spot Information Systems (BSIS) and Moving Off Information Systems (MOIS) for all new type M2/M3/N2/N3 vehicles from July 2022, and for all new registrations from July 7, 2024. These systems are technically defined by UN Regulations R151 (right-side VRU detection) and R159 (front VRU detection at low speeds).

- The “Brussels Effect”: The EU GSR is creating a de facto global standard. Vehicle manufacturers exporting to the EU must comply, and other major markets such as China and the US are developing analogous regulations. This “quasi-GSR” global landscape significantly expands the total addressable market beyond Europe’s borders.

Regional Market Breakdown

The adoption curve and demand drivers vary significantly by region, requiring tailored strategic approaches.

- Europe (~35–45% of Global Demand): The pioneer and most mature market. Demand is driven directly by the GSR mandate. A significant aftermarket is also emerging from local regulations (e.g., London’s Direct Vision Standard) that require retrofits for existing fleets.

- North America (2nd Largest Market): Demand is fueled by “functional equivalence” to EU rules, driven by city-level safety ordinances, stringent school bus safety standards, and pressure from insurance providers. The market is characterized by a high proportion of aftermarket and retrofit installations.

- Asia-Pacific (High-Growth, Top-Tier Market): This region is experiencing accelerated penetration. Demand is dual-sourced: from local regulations for specific vehicle types (e.g., construction vehicles) and from the need for export-oriented OEMs to comply with EU GSR requirements. The penetration of fully compliant systems is currently lower than in Europe, indicating substantial headroom for growth.

Market Sizing and Forecast (2023–2030)

The market is at an inflection point. The initial phase in 2023 was valued at $1.2–1.5 billion, reflecting early adoption and pre-2024 compliance preparations. The period from 2024 to 2030 is expected to see accelerated growth, driven by full enforcement of the GSR and subsequent regulatory alignment in other major markets.

We project that the market will reach $4–6 billion by 2030, representing a compound annual growth rate (CAGR) of approximately 18–25% over the period.

Key Market Trends Shaping the Future (2024–2030)

- Technological Integration and Intelligence: The era of single-sensor (camera-only) systems is ending. Sensor fusion, combining cameras with radar, is becoming the standard to ensure all-weather reliability and reduce false positives. In addition, BSD data is increasingly integrated into higher-level ADAS and autonomous driving domain controllers, becoming a core input for holistic vehicle intelligence.

- Evolving Supply Chain and Business Models: The value chain is shifting beyond pure hardware manufacturing. Deep co-development between Tier 1 suppliers and OEMs is critical for creating differentiated solutions. The growing importance of AI algorithms creates opportunities for software specialists. The business model is evolving toward a “hardware + software-as-a-service” paradigm, enabled by Over-the-Air (OTA) updates for feature upgrades and predictive maintenance, thereby creating recurring revenue streams.

- Cost Reduction and Standardization: Mass adoption will create economies of scale, driving average system costs down by an estimated 30–40% by 2030. This will be accompanied by the emergence of industry-wide standards for interfaces and testing, improving supply chain efficiency, interoperability, and ease of integration.

- Ancillary Demand Drivers: Beyond regulation, fleet safety and risk management are major adoption drivers. Fleet operators are investing in AI BSD as a tool to reduce liability, enhance Corporate Social Responsibility (CSR), and secure lower insurance premiums. Global “Vision Zero” commitments further reinforce this trend, positioning AI BSD as a core enabler of safer logistics and urban mobility.

Conclusion and Strategic Implications

The AI Blind Spot Detection market for commercial vehicles is not a niche segment but a foundational element of the future transportation safety ecosystem. The EU GSR has irrevocably changed the landscape, setting a clear and forceful direction for vehicle safety requirements worldwide.

Strategic takeaways for key stakeholders include:

- For Investors: The market offers substantial growth potential. Focus should be on companies with strong technological expertise in sensor fusion and AI software, and with business models that can adapt to the shift toward software and services.

- For OEMs: Success requires a proactive compliance strategy and deep partnerships with technology providers. The objective is to integrate BSD not as a check-box feature, but as a core, value-adding component of the vehicle’s safety and intelligence platform.

- For Tier 1/2 Suppliers: Differentiation will be achieved through system-level innovation, robustness, and the ability to offer scalable, cost-effective solutions. Partnerships with software and AI firms will be crucial to sustain competitiveness.

In conclusion, the surge in AI BSD is a definitive megatrend. Organizations that anticipate regulatory convergence, master technological integration, and capitalize on evolving business models will be best positioned to lead in this new era of commercial vehicle safety.